Investing for Kids: The Part Most Families Don’t Think About Until Later (Part 2)

Parents are under no obligation to financially support adult children or provide future gifts.

But many families understandably want to help if they can — whether that’s private school fees, university costs, a future house deposit, or simply giving their children a financial head start.

And while the intention is usually straightforward, the way the money is structured can create very different outcomes later around tax, flexibility and control.

One of the more common conversations I’m having lately with high-income families is around helping children financially in the future.

Usually the first instinct is:

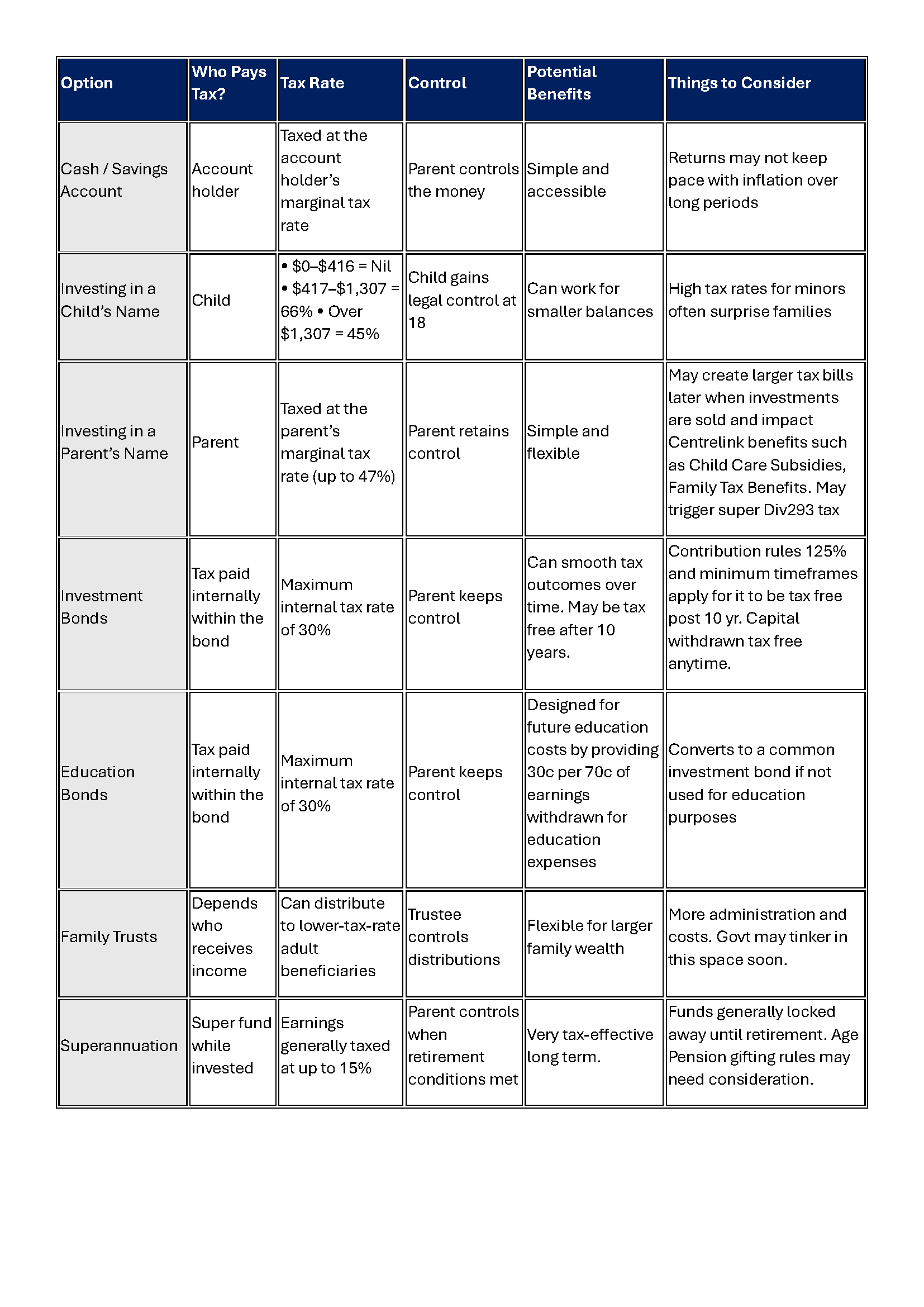

keep the money in cash, or

invest directly in the child’s name.

On the surface, both seem sensible.

But over time, the conversation often becomes less about “what should we invest in?” and more about:

who pays the tax,

how much tax is paid,

and who controls the money later.

I was recently interviewed by the Australian Financial Review on this exact topic because many families are surprised to learn that investment income for minors can quickly be taxed at very high rates:

$0–$416 = Nil

$417–$1,307 = 66%

Over $1,307 = 45%

That often catches families off guard.

Then there’s the control issue.

Once investments are legally in a child’s name, control generally passes to them at age 18, meaning the money intended for education or a future home deposit can potentially be spent however they choose.

That’s why many families instead look at alternatives such as investing in a parent’s name, investment bonds, education bonds or family trusts depending on their goals.

There’s rarely one perfect strategy.

The right approach often depends on:

the purpose of the money,

how much is being invested,

the timeframe involved,

investment risk tollerances,

family income levels,

and how important long-term control is.

Here’s a simple overview of some common approaches families consider

(potential May 2026 budget announcements excluded).

The biggest mistake usually isn’t the investment itself.

It’s setting something up early that no longer fits the purpose later on.

That’s why when I advise families on this matter, I encourage them to first step back and ask:

What is the money actually for?

When will it realistically be used?

Who should control it along the way?

Because often, the best structure isn’t necessarily the one with the lowest tax today.

It’s the one that best balances tax, flexibility, control and long-term family goals.